What You Don’t Know Can Hurt You

When the bills won’t wait and the collectors keep calling, your choices narrow fast. For many people, especially after a layoff, divorce, or medical emergency, taking out a personal loan may feel like the only path forward. But making the wrong choice between a secured or unsecured loan can trap you in a deeper financial hole.

This guide explains what differs in taking out a secured and unsecured personal loans, why it matters if you’re in debt, and how to spot the risks most lenders bury in fine print.

If you’re considering a personal loan to stay afloat, read this first.

What Is a Secured Loan?

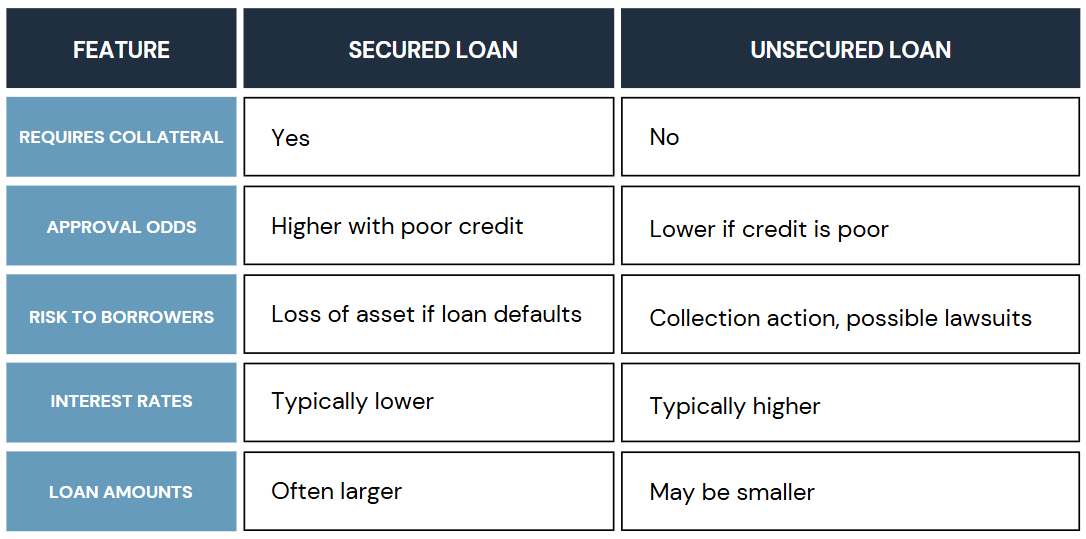

A secured loan is backed by something you own, also known as collateral. This could be your car, a savings account, or even your house. If you fail to make payments, the lender has legal grounds to take the collateral.

Why do people choose secured loans?

-

Easier approval with bad credit

-

Lower interest rates

-

Larger loan amounts

The risk? You could lose your vehicle, savings, or home if you default.

Real-Life Example:

Carlos, a freelance designer in Texas, needed $15,000 to scale his business. His credit wasn’t great, but his car was paid off. He took a secured loan using his vehicle as collateral. When a big client canceled unexpectedly, he missed two payments. The bank gave notice of repossession, putting both his business and transportation at risk.

What Is an Unsecured Loan?

An unsecured loan doesn’t require collateral. Lenders rely on your credit score, income, and repayment history to determine risk.

Why people choose unsecured loans:

-

No risk of losing property

-

Faster application and approval process

-

No collateral required

The risk? You’ll likely face higher interest rates, stricter approval requirements, and aggressive collection efforts if you fall behind.

Real-Life Example:

Amanda and Josh wanted a $25,000 destination wedding but lacked savings. Amanda applied for an unsecured personal loan with a high-interest online lender. They were approved in two days but saddled with a 29.9% APR. After the honeymoon, Josh lost his job. Within weeks, collectors were calling daily. By month three, they were in default.

Secured vs. Unsecured Loans

at a Glance

Hidden Traps in Personal Loan Agreements

Before signing anything, review these key sections of any loan contract:

1. APR (Annual Percentage Rate)

This is the true cost of your loan. It includes interest plus fees. A low monthly payment can still carry a high APR.

What to do: Ask for a breakdown of the APR. Don’t compare interest rates alone. Consider using an APR calculator

2. Prepayment Penalties

Some lenders charge you for paying off your loan early.

What to do: Look for a clause labeled “prepayment.” If it exists, ask if it can be waived.

3. Collateral Clauses

In secured loans, understand exactly what asset is at risk and when it can be seized.

What to do: Ask the lender how many missed payments trigger seizure.

4. Default Terms

Some contracts consider your loan in default after just one missed payment.

What to do: Look for terms like “grace period” or “late payment policy.”

When a Personal Loan Isn’t the Answer

If you’re already receiving collection calls or missing credit card payments, a loan might not solve the problem. It could make it worse. Especially if the loan comes from a predatory lender who is targeting desperate borrowers with misleading terms.

This is where Guardian Litigation Group steps in. We help individuals evaluate their financial and legal options before taking on more debt. Whether that means negotiating with creditors, contesting the debt itself, or understanding your consumer rights, we’re here to protect your financial future.

Personal Loans Q&A

1. Can I switch a secured loan to an unsecured one later?

Some lenders may allow refinancing from a secured to an unsecured loan once your credit improves. However, it depends on the lender’s policies and your payment history. You’ll likely need to reapply and meet stricter credit standards.

2. Do secured loans show up differently on my credit report than unsecured loans?

Both types appear as installment loans on your credit report, but lenders reviewing your credit may note whether collateral was involved. Missed payments on secured loans can result in both credit damage and asset loss, which may be flagged separately in collections.

3. What happens to a secured loan if the collateral loses value?

If your collateral (like a car or investment) depreciates, you’re still responsible for the full loan balance. In the event of default, the lender may seize the asset and still sue you for the remaining balance.

4. Can I use the same collateral for multiple loans?

Generally, no. Most lenders require that the collateral be free and clear. If the asset is already securing another loan, the second lender will likely deny your application or require a second-lien agreement, which carries added risk.

5. Is a cosigner more helpful for a secured or unsecured loan?

A cosigner is typically more impactful for unsecured loans since there’s no collateral to offset the lender’s risk. However, for borrowers with poor credit, combining a cosigner and collateral may open up better loan terms.

6. Are secured loans ever considered safer for the borrower?

Only in very specific situations. If you can confidently afford the payments and have limited credit options, a secured loan may offer better terms without overextending your credit. But “safer” depends entirely on your ability to repay consistently.

7. What type of loan is more commonly used for debt consolidation?

Unsecured personal loans are more common for consolidating credit card or medical debt. However, some borrowers use home equity or auto title loans (both secured) to consolidate higher-interest debts, often exposing themselves to greater long-term risk.

8. How do lenders value collateral for a secured loan?

Lenders usually apply a percentage discount to the market value of your asset to protect themselves. For example, a car worth $10,000 might only secure a loan of $6,000 to $7,000 due to depreciation and resale risk.

9. Are secured loans easier to discharge in bankruptcy?

Secured loans are harder to eliminate in bankruptcy because the lender can still repossess the asset unless you surrender it or pay its value. Unsecured debts are more commonly discharged, especially in Chapter 7 filings.

10. How long should I keep a secured loan before refinancing?

There’s no fixed timeline, but many borrowers refinance once they’ve made consistent on-time payments for 6 to 12 months and have improved their credit score. Refinancing can help remove the collateral requirement and reduce risk.

What If You’re Already Struggling With Debt?

If collectors are already calling and your monthly payments are choking you, a loan may not be the solution yet.

At Guardian Litigation Group, we help clients understand their rights and options before signing anything new. Sometimes that means negotiating with creditors. Other times, it means spotting predatory loan terms that could worsen your situation.

The information provided in this blog article is for informational and entertainment purposes only and should not be construed as legal advice. It is not intended to create, and does not constitute, an attorney-client relationship. Every legal situation is unique, and readers should consult a licensed attorney for advice specific to their circumstances.