When the Consumer Financial Protection Bureau finalized its open banking rule in late 2024, it signaled a meaningful change in how personal financial data may be accessed and shared in the United States. This article explains what the rule is, how it functions in real-world settings, and why it may matter to consumers dealing with credit cards, loans, or broader debt-related concerns as compliance begins in April 2026.

The open banking rule is formally titled the Personal Financial Data Rights Rule. It is a federal regulation issued under Section 1033 of the Dodd-Frank Wall Street Reform and Consumer Protection Act. In general, the rule is intended to establish clearer rights around consumer access to financial data and to create uniform standards for how financial institutions share that data when a consumer authorizes access.

Initial compliance requirements begin on April 1, 2026 for the largest financial institutions, with smaller institutions subject to later phased deadlines.

This rule is important for your consideration as it affects how financial data is handled, how third-party services interact with financial institutions, and how consumer financial profiles are evaluated in debt-related contexts.

How the Open Banking Rule Works and What It Covers

Personal financial data generally includes information related to financial accounts, such as transaction histories, balances, and borrowing activity. This may involve data from credit card accounts, checking and savings accounts, loans, digital wallets, and certain payment platforms.

Under the open banking framework:

- Covered financial companies are required to make personal financial data available when a consumer or an authorized third party requests access.

- Authorized data transfers must be provided electronically and in a standardized format.

- Data access must be offered without charge to consumers or authorized third parties.

- Covered data commonly includes transaction records, account balances, and information necessary to support financial services or payments.

Covered entities typically include large banks, credit card issuers, and other financial service providers that maintain consumer financial data. Smaller institutions may be exempt or subject to delayed compliance, depending on size and regulatory thresholds.

One goal of the rule is to reduce reliance on older data-sharing practices, such as screen scraping, where third parties collect login credentials to access accounts. The rule instead promotes standardized, consent-based data sharing methods designed to improve security and transparency.

Why the Rule May Matter to Consumers

Consumer Control and Financial Choice

In general, the open banking rule may allow consumers to carry their financial data from one provider to another more easily. For example, a consumer evaluating alternative credit card options may authorize a third-party service to review transaction history or payment patterns in order to compare products. This structure is intended to support clearer comparisons across credit cards, loans, and related financial products.

Financial Privacy and Data Use Limits

The rule also places limits on how authorized third parties may use consumer data. Data recipients are generally restricted to using information only for the purpose to which the consumer consented. Using the data for unrelated marketing, resale, or undisclosed purposes may fall outside permitted use under federal standards.

For consumers with debt-related concerns, standardized consent frameworks may replace less secure data-sharing practices and provide clearer expectations regarding how financial information is accessed and used.

Potential Effects on Debt-Related Decisions

Access to organized financial data can influence how consumers evaluate budgeting tools, credit card balances, loan comparisons, or refinancing options. In realistic scenarios:

- A consumer reviewing credit card options may allow a comparison platform to assess transaction and payment history.

- A household considering loan consolidation may rely on third-party tools that analyze balances and payment activity.

In these contexts, personal financial data may support more tailored financial insights. At the same time, how data is interpreted or retained by third parties may affect future lending evaluations or eligibility assessments.

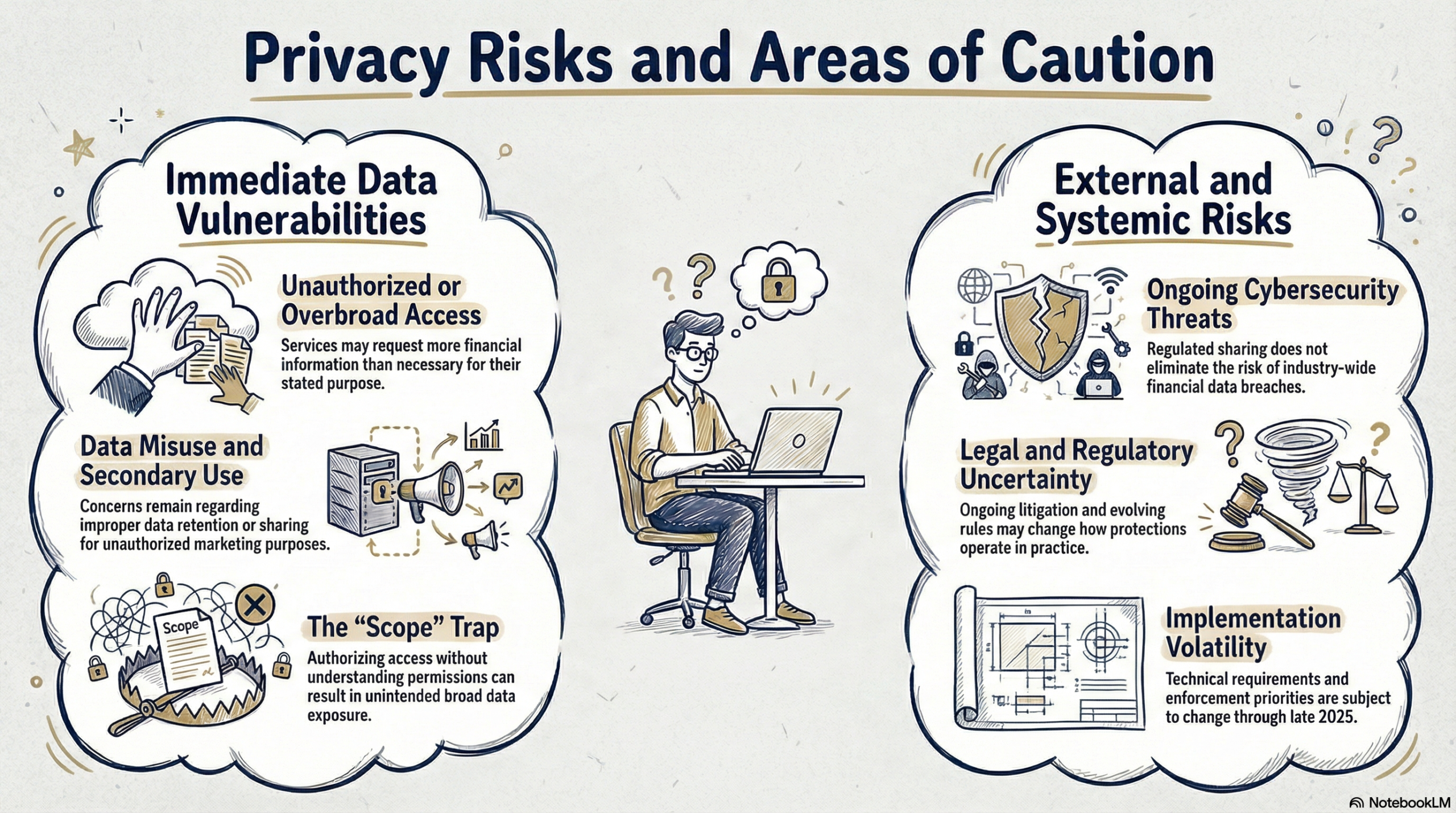

Privacy Risks and Areas of Caution

Even with enhanced data rights, the open banking framework does not eliminate all risks.

Unauthorized or Overbroad Data Access

Authorizing access without fully understanding the scope of permissions may result in broader data exposure than intended. Some third-party services may request more information than is necessary for their stated purpose.

Misuse or Secondary Use of Data

Although federal rules limit how authorized data may be used, concerns remain about improper retention, marketing use, or sharing beyond the original consent. These practices may raise compliance and privacy issues under federal consumer protection laws.

Regulatory Changes and Legal Uncertainty

As of late 2025, aspects of the open banking rule have been subject to litigation and regulatory review. Implementation timelines, enforcement priorities, or technical requirements may evolve, which can affect how the rule operates in practice.

Ongoing Data Security Risks

Data sharing, even when regulated, involves cybersecurity considerations. Financial data breaches remain a risk across industries, and authorized access does not eliminate exposure to security incidents.

Practical Safeguards and Consumer Awareness

The open banking rule places emphasis on informed consent and transparency. Consumers may benefit from understanding:

- What data is being requested and for what purpose

- How long authorization lasts and whether access can be withdrawn

- Which third parties currently have access to financial data

Financial institutions increasingly provide tools that display authorized data connections, which can help consumers maintain awareness of how information is shared.

Realistic Consumer Scenario

Consider a consumer with multiple credit card accounts evaluating whether combining balances into a single loan could affect monthly payment structure. Under the open banking framework, the consumer may authorize a financial planning service to review recent transaction and balance data in order to generate comparative information about available loan products.

In this scenario, the value of standardized data access depends on how the service uses and protects the information. Clear disclosures, limited authorization scopes, and defined retention practices may reduce some risks when compared with older data-sharing methods. At the same time, unclear or overly broad privacy terms could signal potential concerns.

People Also Asked

-

Does the CFPB open banking rule apply to all financial institutions?

In general, the rule applies first to the largest financial institutions, with smaller institutions subject to later compliance phases. Some providers may be exempt depending on size and regulatory thresholds. Coverage can vary based on how the rule is implemented.

-

Can open banking affect how lenders view a consumer’s financial profile?

Authorized financial data may provide lenders or financial tools with a more detailed picture of transactions and balances. This information can influence how financial products are evaluated or presented. Outcomes may vary depending on how data is interpreted.

-

Is open banking intended to help consumers manage debt?

The rule is designed to improve data access and transparency rather than directly address debt balances. Some consumers may find that clearer financial data supports informed comparisons. However, debt outcomes depend on many financial factors.

-

Are third-party budgeting or comparison tools regulated under open banking rules?

Third parties accessing data under the rule must comply with federal data use and consent limitations. Their obligations focus on how data is accessed and used rather than guaranteeing specific financial results.

-

Can consumers revoke access once financial data is shared?

The rule emphasizes consumer consent and the ability to withdraw authorization. How revocation works can depend on the financial institution and the third-party platform involved. Processes may vary by provider.

-

Does open banking change existing consumer protection laws?

The rule operates alongside existing federal consumer protection laws. It does not replace laws related to credit reporting or fair debt practices, which continue to apply separately.

-

Could open banking increase financial privacy risks?

While the rule introduces safeguards, sharing data with more entities can increase exposure. Consumers may still face risks related to data misuse or cybersecurity incidents, depending on how information is handled.

Conclusion

The CFPB’s open banking rule and the April 2026 compliance milestone represent a shift in how personal financial data may be accessed, shared, and protected. For consumers navigating credit cards, loans, or debt-related decisions, the rule may offer greater transparency and standardized safeguards when authorizing third-party access to financial information.

However, expanded data access also brings responsibility and risk awareness. Understanding how consent works, how data is used, and how protections vary under federal and state law remains important as implementation unfolds.

For those seeking clarity about data access, privacy, or potential legal exposure, consumer education materials and official guidance from agencies such as the Consumer Financial Protection Bureau can help provide context and understanding.

The information provided in this blog article is for informational and entertainment purposes only and should not be construed as legal advice. It is not intended to create, and does not constitute, an attorney-client relationship. Every legal situation is unique, and readers should consult a licensed attorney for advice specific to their circumstances.